Next-generation geospatial data to support the future of insurance

-

Comprehensive coverage

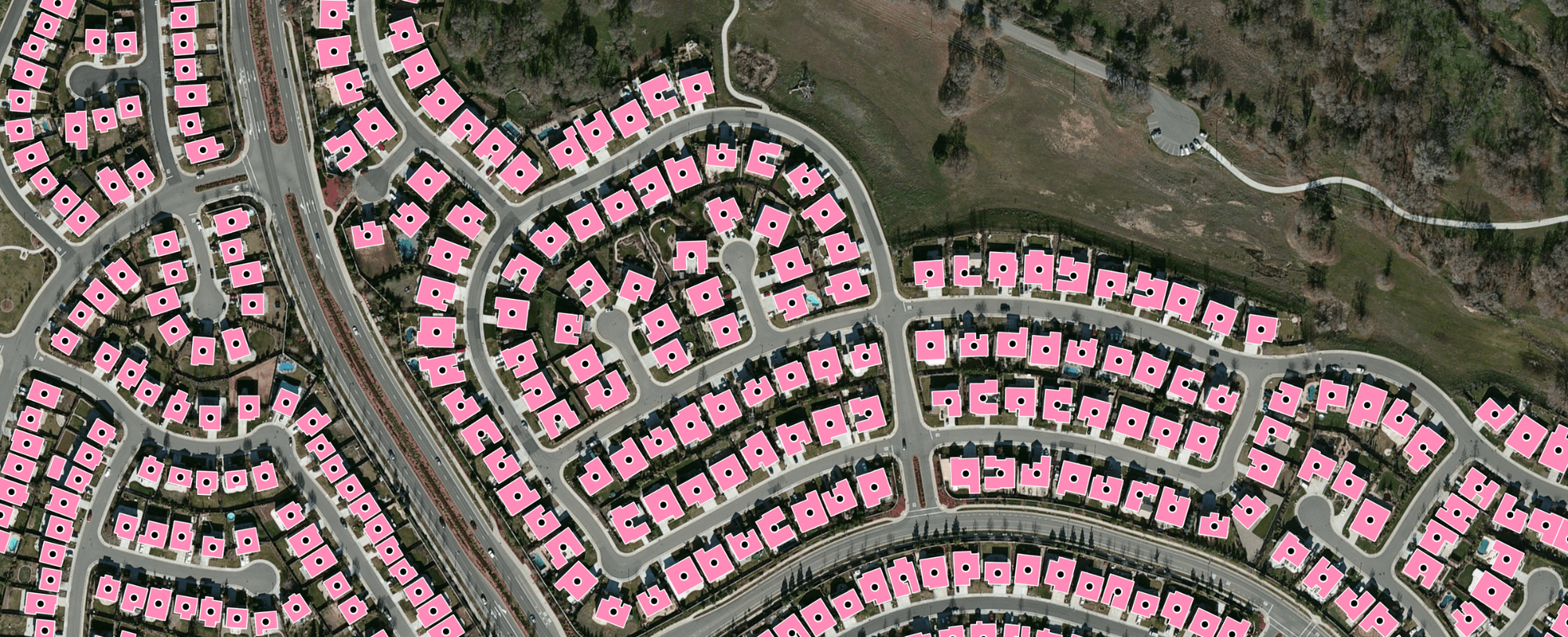

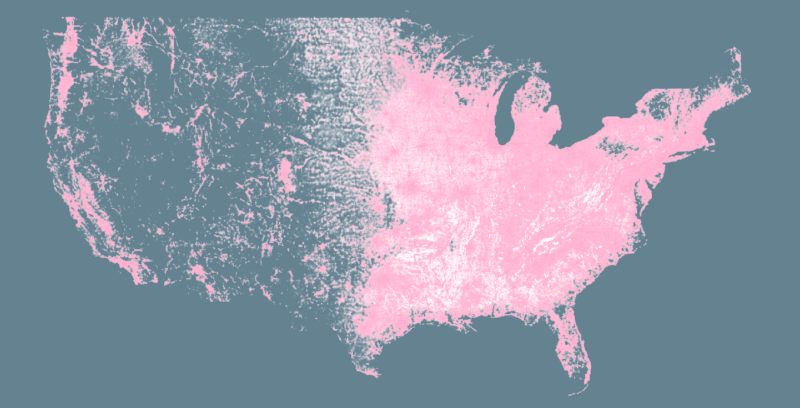

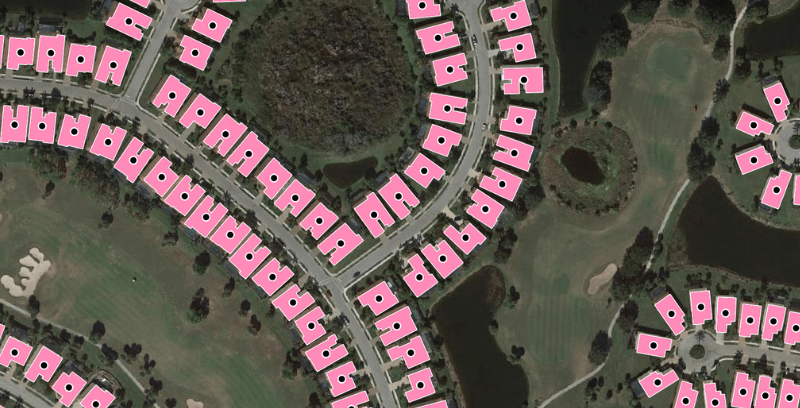

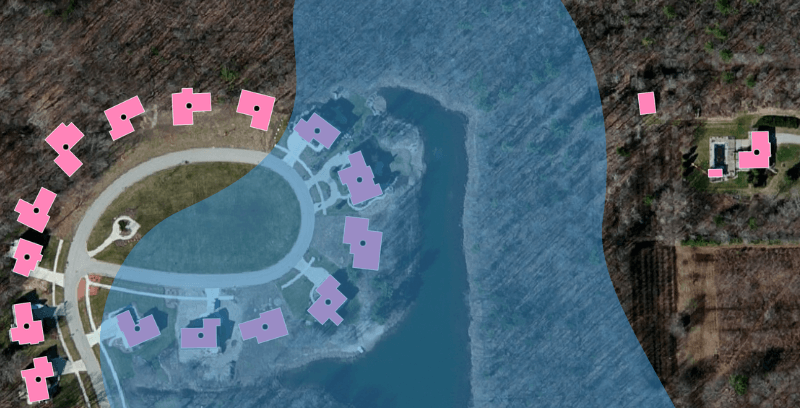

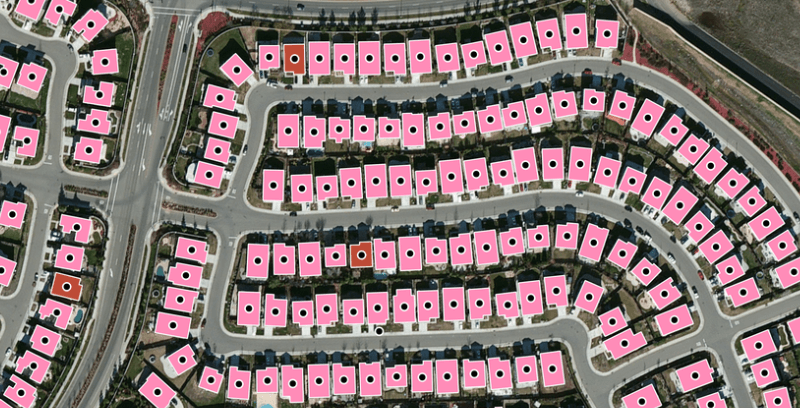

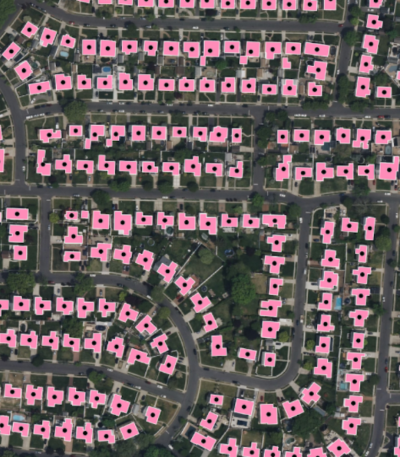

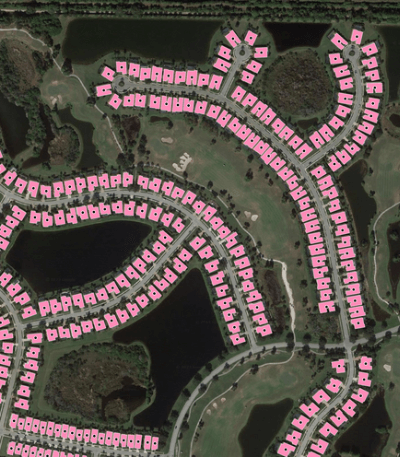

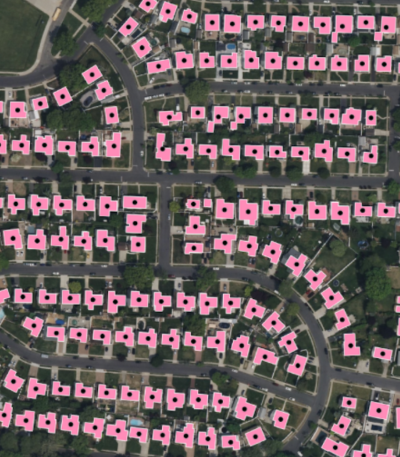

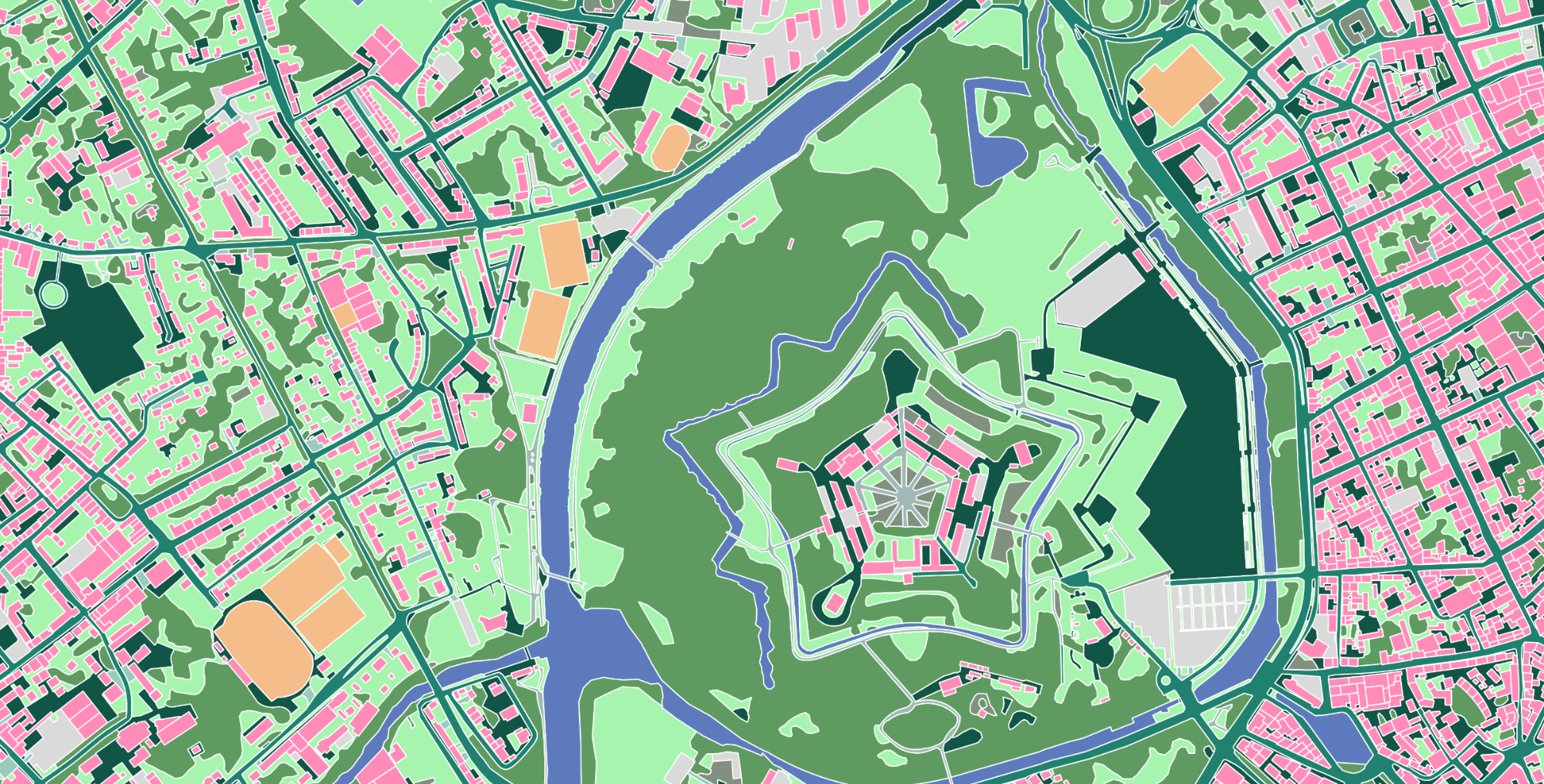

Ecopia® developed the first and only complete map of every building in the US, comprising 178M+ buildings and 270M+ primary and secondary addresses, to provide insurers with a source of truth for property analytics. Our AI-based mapping technology extracts insight from geospatial imagery at a national scale, from dense urban centers to sparsely populated rural areas.

-

Accurate geocodes

Ecopia has developed a dedicated geocoding engine which uses a unique machine learning-based address parsing system to match each address to the correct building at-scale. This results in accurate building-based geocoding, offering a uniquely accurate foundation for all subsequent location-based analyses.

-

Fresh insights

The real world is constantly changing, perpetually impacting property risk and replacement costs. Ecopia leverages our AI-based mapping systems to continuously ingest and process fresh high-resolution geospatial imagery, ensuring we are providing the most accurate representation of reality.

Insurance Use Cases

-

Underwriting

Avoid scenarios of under- or over-pricing policies by accurately mapping each address in your book of business to high-precision building footprints.

-

Claims

Streamline claims management workflows by analyzing the building(s) and surrounding property related to each address in your book of business.

-

Risk Assessment

Develop a comprehensive view of a property and its surroundings to better anticipate risk and estimate replacement cost.

Trusted by industry leaders

With Ecopia, Harford Mutual has been able to reduce time spent on manual property assessments by 75%. Partnering with Ecopia allows our underwriters to move quickly without sacrificing quality as we grow our book of business - that alone makes the investment worth it.

We chose to partner with Ecopia after thoroughly evaluating various building footprint sources for the United States on metrics of comprehensiveness, accuracy, and recency – and I am also convinced that Ecopia will extend this competitive edge with future products for the industry.

As a result of the integration of Ecopia’s Building-Based Geocoding, Tokio Marine North America Services was able to move to a true building-based database of policies, resulting in the ability to better estimate reconstruction cost and risk.

We are proud that our partnership with an industry-leading company like Ecopia can push the boundaries of AI-driven underwriting to create next-generation flood insurance solutions for our customers.

We are very excited to work with Ecopia to leverage their geocoding and building footprint data. Their building centroid is among the most accurate in our test of several options, and we've enjoyed their easy-to-use API and strong customer support.

We take pride in advanced integrations, with Ecopia’s geospatial technology being a huge addition. We will better understand individual property flood risk, and are thrilled to incorporate Ecopia’s industry-leading Building Based Geocoding.

The coverage and precision of Ecopia’s geocoded building footprints enable our user base of independent agents to provide competitive and customized quotes to homeowners more efficiently and confidently than ever before.

Learn more about Ecopia's insurance solutions

News

Insurance

Farmers Insurance to Leverage Ecopia's Building-Based Geocoding for Insurance Decision-Making

News

Insurance

Ecopia AI Enhances Building-Based Geocoding with Flood Zone & Change Detection Insights

Case Study

Insurance

Optimizing Reinsurance Strategy with Building-Based Geocoding

News

Insurance

Standard Casualty Selects Ecopia AI’s Building-Based Geocoding to Support High-Precision Property Intelligence

Case Study

Insurance

Leveraging Ecopia AI's Building-Based Geocoding to Enhance Replacement Cost and Risk Estimation

News

Insurance

Openly Selects Ecopia AI’s Building-Based Geocoding to Power Accurate Risk Assessment for Underwriting

News

Insurance

Harford Mutual Insurance Group Partners with Ecopia AI to Enable More Accurate and Efficient Risk Assessment

News

Insurance

Neptune Flood Enhances AI Engines with Ecopia's Building-Based Geocoding

News

Insurance

Ecopia AI Named as a Leading Innovator in the InsurTech Sector

News

Insurance

Flow Flood Chooses Ecopia AI’s Building-Based Geocoding API for High-Precision Flood Insurance Underwriting

News

Insurance

SageSure Selects Ecopia AI’s Building-Based Geocoding to Enhance Location Intelligence

Ready to get started?

Get in touch with our team and explore our data portal.